Why Turkish Banking Sector?

TURKISH BANKING SECTOR

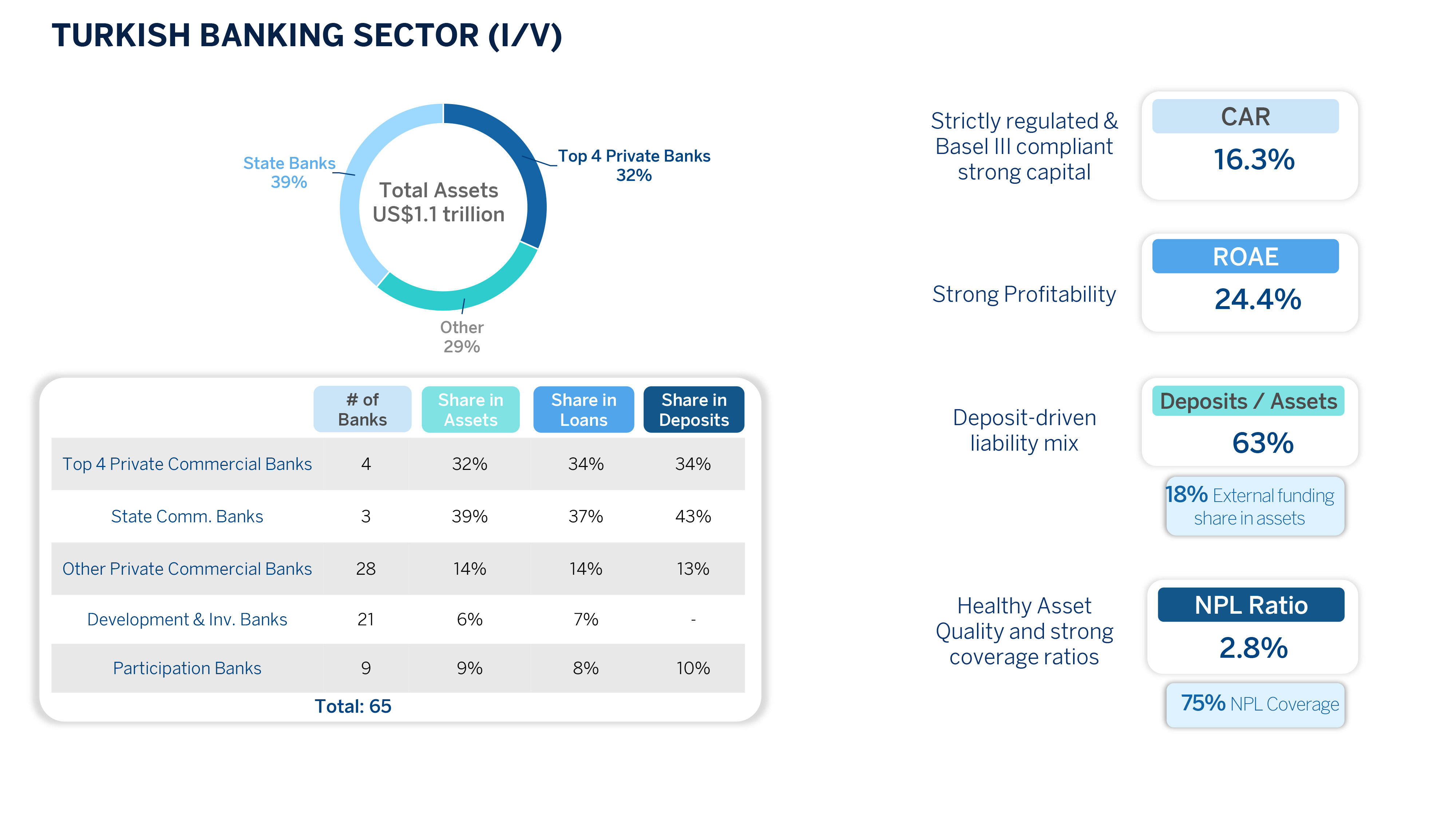

Note: Sector figures are based on bank-only BRSA monthly data as of March 2026

Number of banks figures are based on BRSA monthly data, excludes banks under SDIF and Ziraat Dinamik Bank (Digital bank)

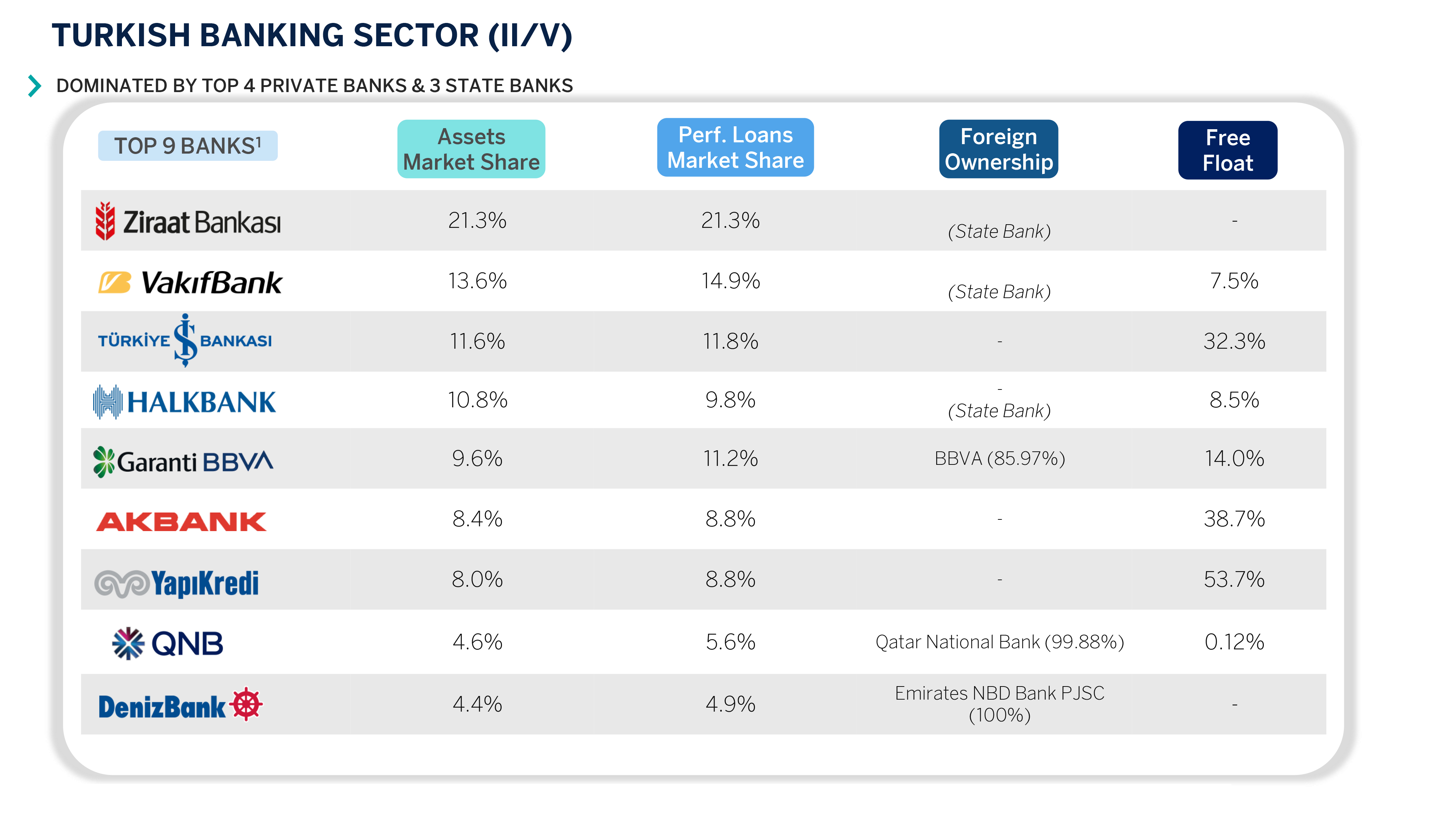

Note: Sector figures are based on bank-only BRSA monthly data as of March 2026.

1 Top 9 banks make up 77.2% of sector’s total asset as of March-26 in sector. Assets and loans market shares are among commercial banks.